The high risk

faced by customers at this time encourages the development of Islamic Banks. Islamic Banks are less risky

and more resilient than their counterparts, due to the aspects of their bank

capital requirements and mobilisation of deposits. As opposed to Conventional

Banking, depositors to Islamic Banks are entitled to be informed about what the

bank does with their money. They also have a say in where their money should be

invested. Islamic banks also strive to avoid interest at all levels of

financial transactions and promote risk-sharing between the lender and

borrower.

Islamic Banking is not just for Muslims. It’s for everyone. Do not let the name cloud you. It’s like how

Häagen-Dazs

is neither German nor European; or how Superdry is not from Japan. It’s simply

a term.

However,

it does represent something – Transparency and Risk sharing. . Now comes Hada

DBank.

What’s HADA DBANK?

HADA DBank is a digital Islamic Bank that offers fewer

risks than Conventional Banking. We are the first Digital Bank to fuse Islamic

Banking Module with Blockchain Technology, to create an ethical and responsible

banking ecosystem.

We have learnt from the pitfalls of modern financial

institutions, and that is why we chose Islamic

Banking to forge the future. Islamic Banking principles

require total transparency from both the

customers and the bank. We aim to promote ethical and

responsible banking globally.

HADA DBank is

developing a comprehensive Blockchain digital bank that will make life easier

for everyone, regardless of their statuses.

Our customer will be able to perform banking activities

with 0% fees and enjoy quality services from

us. We are here not to just profit, but rather to make

justified profit while ensuring a better banking

experience.

Our Headquarters will be based in Zug, Switzerland – the

Crypto Valley of the world.

Swiss Financial Market Supervisory Authority FINMA:

FinTech Licence

Bank of England Prudential Regulation Authority and

Financial Conduct Authority:

New Bank Start-Up Unit license

Other Countries: E-Money Licenses

Now, why Islamic Bank?

The

reason is, we aspire to be a ‘just’ organization in the financial industry. Islamic

banking, due to its transparency, profit and loss sharing concept, will

minimize market manipulation and eliminate another domino crash.

The

demand in Islamic banking is tremendous. There are 1.7 billion Muslims

worldwide, and this

number

is growing.

According

to World Bank, the Islamic financial industry has expanded rapidly over the

past decade, at

10-12%

annually.

Market

Our market will focus on the 1.7 billion Muslims globally. A more narrowed focus in this market will be the ASEAN population.

South Asia and East Asia and the Pacific together account for more than half the world’s unbanked adults. South Asia, home to about 625 million adults without an account, has about 31 percent of the global total; East Asia and the Pacific, with 490 million unbanked adults, accounts for about 24 percent.

The world’s unbanked adults by region

Adults without an account (%), 2014

Share of the world’s unbanked adults in China, India, and Indonesia

Adults without an account (%), 2014

There is a interesting fact about ASEAN

- It has an unbanked population of approximately 438 million.

- More than half of ASEAN’s population is under the age of 30.

- It has a market penetration of 854 million smartphones, or 133% compared to its population; but only 53% of ASEAN’s population is online, which leaves significant room for market expansion in the future.

According that fact, makeus to focus on ASEAN as our secondary market.

Exclusive

Features And Advantages

- Free Encrypted Account & e-Wallet

- Saving & Withdrawal

- Transfer, Remittance & Exchange

- Loan & Investment

- Real-Time Payment

Bot & AI

- Bot HADA - Financial Management Bot/ Personal Financial Assistant (HUDA)

- AI (Artificial Intelligence)

Personal Financial Advisor (HADI) (Basic)

Helps you to invest by providing unbiased financial advice

Chasback and discount are rewaded when using our Debit Card, either phisycal or virtual for the 1th year and forever paying by using HADAcoin.

Points System

Collect points from your spending with our e-Wallet or Debit Card and convert it to cash or cryptocurrency/ token to spend more.You may also use the points collected to redeem anything you like onour partners’ e-Mall or physical outlets worldwide.

Bonuses and Bounties

Referral Bonus or Bounty when your referrals register with us

through your Referral Code.

HADACoin & your Savings are backed by valuable assets such as Precious Metals & insured according to Islamic Banking Principles for your peace of mind.

HADACoin

Buyers will be able to use HADACoin to perform banking transactions or daily activities. Our customers will be issued with a Debit Card, which enables them to perform transactions with our HADACoin, within our banking platform or other merchants globally.

A total of 500 Million HADACoins will be issued. 295 Million coins will be offered for sale. Out of the

295 Million coins, 20 million will be allocated for private investors and institutional buyers. 50 Million

of the 275 Million coins will be released during PRE-ICO exercise and the remaining 225 Million coins

will be released in our ICO exercise in the near future. 10 Million coins will be allocated for the bounty

campaign.

HADACoin is a ERC-20 coin created using Ethereum platform. A total of 500 Million HADACoins will be

created. HADACoins will have 6 decimal units. Further info about HADACoin as stated below:

- It has no intrinsic value nor it is a security,

- There is no guaranteed Monetary Profits such as Dividend, Return or anything related when buying our Coin as it is,

- You can use your Coins to:

- Perform financial activities and services on our Banking Platform,

- Pay for services using our Debit Card,

- Receive Monetary Profits such as Dividends, Returns and anything of equivalent by keeping it in our Savings Account or utilize our Investment Solutions

- Act as a collateral when you apply for our Unsecured and Term Loans

- Trade it on Crypto-Exchanges and make more profit by increasing HADACoin’s value

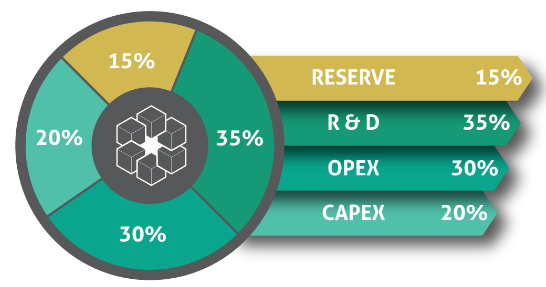

Allocation

Roadmap

Technology

HADA DBANK employs a private blockchain which is stored on every node in the network. By default,

the nodes are all controlled by HADA DBANK. Some nodes only store a copy of the blockchain and do

not take part in the transaction confirmation process (consensus protocol).

The main database of the core is implemented in a blockchain structure, where each block is a set of

transactions. Every new block defines a new state of the core according to the previous block’s state. In addition to the main database, there is another database that stores only the final state of the core. This database is optimized for fast reading and writing of account data during validation of new transactions.

HADA DBANK architecture consists of different components where each component is handling a

separate set of functions. This makes it easier to modify each of the components independently by expanding or adding new features, as well as design and launch new platform components. Interaction between platform components is performed through the message or request exchange, which is being broadcast over network channels.

A decentralized network of specialized computers validates and confirms transactions. In a general

case, these computers are under the control of HADA DBANK. Any transaction which was confirmed by the core is irreversible as it is stored in chronological order in the blockchain; even if its initiator can prove that transaction was unwanted or mistaken.

Therefore, we created HADA DBANK with the intention to make it easy and simple for everyone to

perform banking activities regardless of their social status. HADA DBANK will impose strict KYC procedures to hinder fraud and money laundering

Scheme of component relations in HADA DBank platform

Transaction processing in HADA DBANK platform

Scheme of precessing and updating the main database ( blockchain)

HADA DBank platform core components

.

Examples of usage: Account Balance Reload & Remittance

- For:

- Smartphone : Download the HADA DBank app or

- SMS : Fill-up a form at any participating outlets to create an account;

- Reload their account and maintain a minimum amount annually to stay active;

- Start sending money to any available channels on the app/ SMS system;

- Sender will receive a unique code to confirm remittance on the app/ SMS system;

- Receiver will receive a notification on the remittance;

- Sender will receive a “Remittance Successful/ Unsuccessful” notification and a receipt.

Management Team

Advisors

Strategic Partners

Media Partners

As Seen In

For more informatin, you can visit:

Website : https://www.hada-dbank.com/

Ann Thread : https://bitcointalk.org/index.php?topic=2607739.0

Author : ririsw

Tidak ada komentar:

Posting Komentar